Blog Post: Opportunities of FinTech in Canada

As early stage FinTech investors, we are not only excited about the North American market, but are particularly excited about Canada’s potential to be a top tier FinTech hub.

Although much of the public attention in Canada is on the largest “Big 6 banks”, there are many other financial institutions in Canada. The Office of the Superintendent of Financial Institutions (OSFI) regulates 386 Canadian and foreign financial institutions doing business in Canada (of which 32 are Canadian banks and 123 are Canadian insurance companies). With over 35 million Canadians, our country operates in a less fragmented market in comparison to the U.S. where there are over 9,000 financial institutions that could serve over 320 million Americans. However, we think Canada has an interesting mix of regionally-focused (like credit unions and smaller insurance companies), nationally-focused domestic and international participants. There are multiple ways for FinTech companies to achieve product-market fit and scale here!

Toronto is the home to Information Venture Partners and is one of the top financial centres in North America. The surrounding financial hubs within a short flight of Toronto offer FinTech start-ups something that Silicon Valley cannot: proximity to the largest concentration of financial institutions in the world. These institutions represent a huge potential customer base, domain-specific talent and a partner in the commercialization of innovation in these major institutions. Coincidentally, in our FinTech universe, of which we are tracking almost 400 companies across Canada, almost 50{0573984a2b8f609c30111d9663e55dcffe5bf46757f544e848868cbca776ed36} of these companies are in Ontario.

A promising FinTech cluster is also developing in other areas of Canada. Quebec employs 232,500 employees in the financial sector. Leading banks such as National Bank, Laurentian, and Desjardins are major supporters of the evolving FinTech ecosystem in Quebec. Additionally, British Columbia employs 155,900 people in the sector and is considered to be the global gateway to the Asian financial markets.

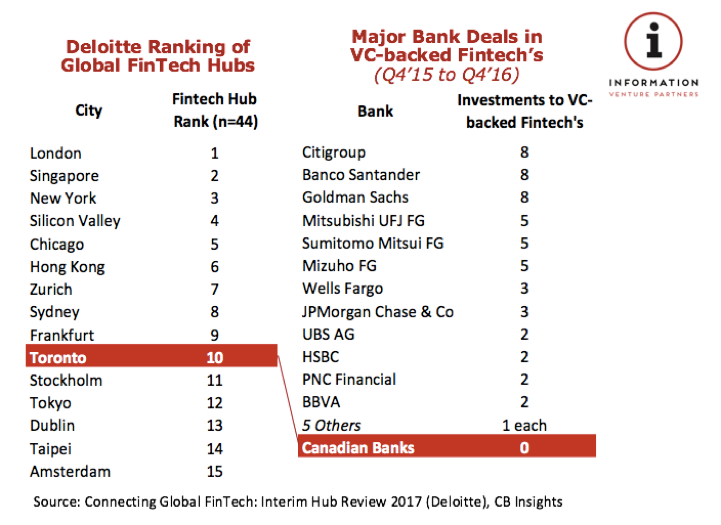

Toronto was ranked 10th amongst global FinTech hubs (Deloitte, April 2017), and was ranked “excellent” in the city’s “proximity to customers” and “proximity to expertise”. However, that is in sharp contrast to reported bank direct investments into VC-backed FinTech’s as per CB Insights.

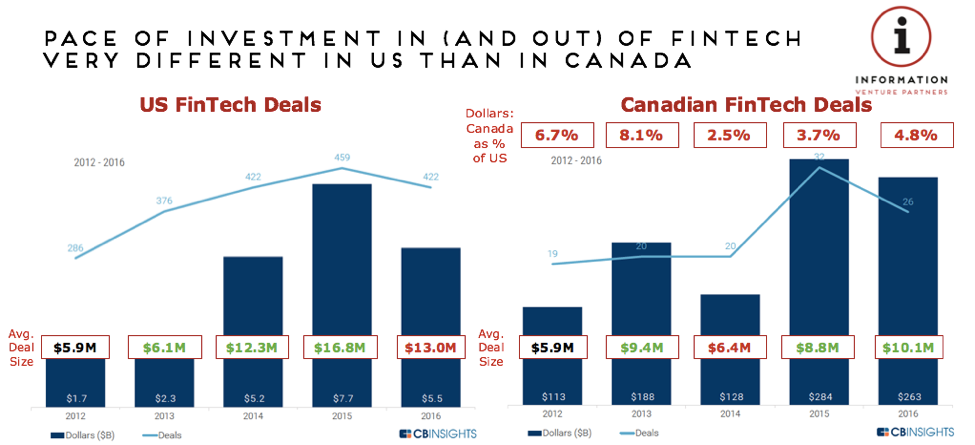

Including VC activity, we are still encouraged by a boost in FinTech investing in Canada, but this lags behind our U.S. counterparts significantly. Although the number of deals and dollars invested into Canadian FinTech decreased year-over-year in 2016, we note that the average deal sizes in Canada are actually trending upwards ($10.1M in 2016 vs. $8.8M in 2015), but are trending lower in the U.S. ($13.0M in 2016 vs. $16.8M in 2015).

While VC activity into U.S. FinTech may cool off, we expect Canada to buck the trend. Being seasoned FinTech investors, we have seen startups demonstrate a greater level of domain and market knowledge, founder and team maturity and incumbent-startup partnerships.

We are spending more time discussing this topic at the Empire FinTech Conference in Toronto on June 27. If you want to learn more about this event and save 10{0573984a2b8f609c30111d9663e55dcffe5bf46757f544e848868cbca776ed36} on tickets to this event, link here (discount code: SPEAKFINTECH10).

Rob